Good news – Super contribution caps to rise

On 1 July 2021, both the concessional and non-concessional superannuation contribution limits, also known as ‘super contribution caps’, will rise.

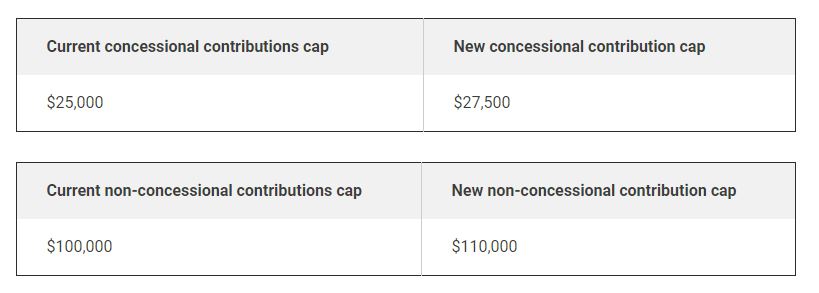

This is good news because this is the first time these limits have changed since 1 July 2017, when the concessional contributions cap was reduced to $25,000 pa for the 2017/2018 financial year and onwards.

Since that time, the non-concessional contribution cap hasn’t changed either, currently $100,000 pa.

What are Concessional contributions?

These are super contributions made by your employer, from your pre-tax income (salary sacrifice contribution) or contributions for which you claim a tax deduction. They are generally taxed at only 15 per cent instead of your marginal tax rate.

What are Non-concessional contributions?

These are super contributions made from your after-tax income. Since you’ve already paid income tax on these contributions, they are tax-free going into your super.

Due to indexation of Australians’ average weekly ordinary time earnings (AWOTE), the concessional cap will increase to $27,500 from 1 July 2021.

What are the current and new contribution caps?

What does this increase mean for you?

Any increase in the super contribution caps means you may increase how much you can contribute to super. The tax benefits plus the compounding of returns can make a substantial difference to your final super benefit.

Additional concessional contributions to super can be made by ‘salary sacrificing’ through your employer or via ‘personal deductible contributions’.

You should consider whether to make non-concessional contributions or maximise your concessional contributions.

Concessional contributions

Additional concessional contributions can reduce your taxable income and your end-of-year tax liability. Concessional contributions are subject to just 15% tax on entry to your super fund compared to your upper marginal tax rate which could be as high as 37% or 45% (plus 2% Medicare levy) if you’re in one of the highest tax brackets.

Note: an additional 15% tax may apply to concessional contributions if your income is over $250,000.

How to make concessional contributions

Additional concessional contributions to super can be made by ‘salary sacrificing’ through your employer or via ‘personal deductible contributions’. Both methods have the same tax benefit so the method you choose comes down to what suits you:

Salary sacrificing comes out of your pre-tax salary and reduces your net taxable income meaning you may pay less tax on your personal income.

Personal deductible contributions are paid by you, and you can then claim a tax deduction when completing your tax return. If you choose this method, you need to submit a form to your super fund by a certain time advising your ‘intent to claim a deduction’ on your super contribution.

Making the most of ‘catch up’ contributions

‘Catch up’ contributions may allow you to use up to five previous financial years’ unused contribution caps in the current financial year if you meet certain requirements. The 2018/19 financial year was the first financial year you could accumulate unused concessional contributions. Unused carried forward concessional cap amounts expire after five years.

Non-concessional contributions

Non-concessional contributions do not entitle you to a tax deduction, but you won’t pay any additional tax as you’ve already paid tax via your personal income tax liability. Earnings on the contributions are taxed at only 15% and are tax-free once you access them as either a lump sum or a pension after age 60, when you satisfy a condition of release such as retirement.

Making non-concessional contributions to super might benefit you if you are seeking to contribute larger lump sum contributions.

Making the most of the ‘bring forward rule’

If you were age 64 or less at 1 July 2020 you may be eligible to use the ‘bring forward rule’, ie bring forward and use up to two future years’ worth of your non-concessional contribution caps.

Depending on your total superannuation balance this may allow you to contribute up to $300,000 (3 x $100,000) into super this financial year. However, if you wait and the cap increases from $100,000 to $110,000, the bring forward amount will increase to $330,000 next financial year.

You generally need to meet a ‘work test’ if you are 67 to 74 years old at the time of contribution.

Legislation is pending to increase the age at which you can trigger the bring forward rule from age 64 or younger as at 1 July of the relevant financial year to age 66 or younger.

With increases in the contributions caps on the horizon, 2021 may be a good year to revisit how much you are contributing to super and make a super plan for the future.

Bronson Financial Services

“At a time of industry upheaval, the support of Capstone has been a godsend. Everything they promised they delivered.If you are looking for a new licensee you cannot beat the Capstone service offering."

Canyon Financial Planning

“Capstone Financial Planning should be at the top of your list for a Licensee. Grant and his amazing team give a down to earth and personalised approach to supporting practices.”

Strategic Retirement Solutions

“I recommend Capstone to any adviser seeking to 'go out on their own'. They are a fabulous licensee!”

Everalls Wealth Management

“With Capstone I can operate my business free from conflict. They have no in-house products, a flexible APL, and an extensive list of SMA solutions. I recommend Capstone highly.”

Nett Assets

“I can highly recommend Capstone for planners seeking an independent licensee that’s not in your face but provide quality support services. Their service and support is second to none and has allowed us to concentrate on providing our clients with a premium level of service.”

Paradigm Principle

“Having been with Capstone for a number of years, one thing that really stands out is their willingness to help and can do attitude. These are qualities we really appreciate.”

IEC Advisory

“The team at Capstone are all genuinely really good people. They are remarkable with their service culture. They really do care what you think, and they are genuine about our joint success into the longer term.”